As we start another year, the time has come to start updating and setting your financial goals. Whether they be long-term such as planning for your retirement, or short-term such as minimizing your tax burden for the 2024 tax year, RRSPs & TFSAs can play an important role in your financial planning process. However, the question that comes up time and time again is which is better, the RRSP or the TFSA? While both are great, it is important to understand how and when to use each account. Here is your guide to help break down the accounts.

Understanding the RRSP & TFSA

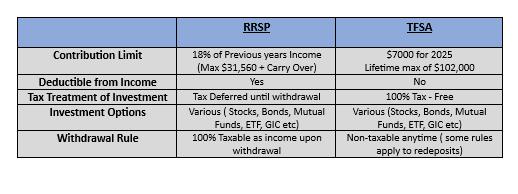

RRSP:

A Registered Retirement Savings Plan otherwise known as the RRSP is a savings plan registered with the federal government that you contribute to for retirement purposes. When you contribute money to an RRSP, contributions are tax-deductible, meaning that they can be deducted from your current year (or previous year if the contribution is made within the first 60 days of the following year) tax return reducing the total amount of income taxes you pay. Furthermore, any investment income, dividends or capital gains earned from investments held within the RRSP grow tax-deferred, as long as the money remains within the RRSP. Upon withdrawal ( likely in retirement), the funds become fully taxable as income.

TFSA:

The Tax-Free Savings Account otherwise known as the TFSA, is a savings plan also registered with the federal government that allows Canadians to save for either short or long-term goals. Unlike the RRSP, TFSA contributions come from after-tax dollars and do not provide a deduction against your income taxes. However, the growth, interest, dividends etc. are completely tax-free during its lifetime and also upon withdrawal. Annual limits for the TFSA are set by the Federal government, but all unused room can be carried forward indefinitely. The contribution limit for 2025 is $7,000.

A Registered Retirement Savings Plan otherwise known as the RRSP is a savings plan registered with the federal government that you contribute to for retirement purposes. When you contribute money to an RRSP, contributions are tax-deductible, meaning that they can be deducted from your current year (or previous year if the contribution is made within the first 60 days of the following year) tax return reducing the total amount of income taxes you pay. Furthermore, any investment income, dividends or capital gains earned from investments held within the RRSP grow tax-deferred, as long as the money remains within the RRSP. Upon withdrawal ( likely in retirement), the funds become fully taxable as income.

RRSP VS TFSA

Which is better: RRSP or TFSA ?

Which is better: RRSP or TFSA ?

Choosing between the RRSP and the TFSA can be confusing. In an ideal world, we would like to be able to contribute to both, but sometimes reality often prevents us from doing that. If you are choosing between the two, it is important to assess your personal needs and your financial situation. Here are a few general guidelines to consider before making that decision.

Income & Tax Bracket: As a general rule of thumb, the higher the income and tax bracket, the more one should favor the RRSP. For high income earners, the tax savings can exceed 50% making the contribution quite beneficial in reducing the income tax burden. For lower income earners, the tax savings would be less, often making the TFSA more attractive. We suggest consulting with your team of professionals to run some calculations to help you decide the appropriate strategy.

Time Horizon & Need for Liquidity: The time horizon for your savings will have a significant impact on which type of account to choose from. While RRSPs are generally geared for long-term/ retirement purposes, the TFSA can be used towards both short-term and long-term needs. As RRSP’s are fully taxable upon withdrawal, the idea is to withdraw them when your income is lower (retirement) to benefit from the income gap during your working years. As the TFSA has no tax consequences upon redemption, this is often better suited for short-term needs.

Are you saving for a Home or Continued Education? While the RRSP is designed for retirement savings, there are 2 cases where using the RRSP for short-term needs can be extremely beneficial.

- Home Buyers Plan (HBP): With the HBP you can take up to $60,000 tax-free out of your RRSP to put towards the purchase of your first home. The funds must be repaid over 15 years, starting in the second year after which the withdrawal was made. If you qualify, for the HBP this can provide both a tax deduction for your income taxes and funds for the down payment.

- Life Long Learning plan (LLP): With the LLP you can take up to $20,000 ( $10,000 per year for 2 years) towards continued education or pursuing your studies. This can also be withdrawn tax- free, but must be paid back over 10 years.

While the optimal saving strategy for a home or education will be to combine RRSP and TFSAs, we generally recommend using the limits available above first and then topping it up with your TFSA.

Group Plans or Work Matching: Are you working for a company or belong to an association that offers group RRSPs, pensions or any employer matching programs? If yes, the attraction towards the RRSP becomes even more significant. Generally, under such arrangements, the employer will match contributions as a percentage of your deposits. For e.g., an employer may match dollar for dollar up to 5% of your salary. On a $100,000 salary that would be an extra $5,000 added to your RRSP, on top of the $5,000 you deposit. This is free money added to your account, that would be virtually impossible to earn through investing. If this is something that is available to you this should almost always be maximized.

Want to know more?

The RRSP vs TFSA discussion is very specific to individual needs and personal situations. While following the guidelines above can help with the decision-making process, we suggest consulting a professional before proceeding with any form of investment. Furthermore, no investment should be made without understanding the risks associated and without a proper plan in place. We can help determine if you should contribute to an RRSP, TFSA, or both.

Reach out to our team of specialized advisors and we can help you make the right decisions to support your financial goals.